As our world grows increasingly digital, banking and fintech are redefining how we access and manage money. But in this fast-paced evolution, one critical factor stands out: accessibility. Digital accessibility in finance goes beyond meeting regulations. It’s a decisive factor that can make or break user adoption. Accessibility is a powerful catalyst, opening opportunities for millions, expanding markets, and reshaping brand loyalty.

Globally, over one billion people live with some form of disability, and in the U.S. alone, people with disabilities control over $645 billion in disposable income. These numbers represent more than just a consumer segment; they underscore a significant business opportunity waiting to be unlocked. For aging populations, people with disabilities, and underserved communities in emerging markets, accessible banking can bridge critical financial gaps, providing not only financial services but financial empowerment.

The journey toward digital accessibility in banking is not merely a response to mandates but a step toward a more inclusive economic future. As financial institutions strive to adapt to a rapidly digitizing landscape, they face a pivotal choice: either design for inclusivity and capture a wider, more loyal customer base or risk excluding entire demographic groups who need these services most.

This article explores how accessible banking can redefine customer loyalty, reduce churn, and create lasting growth, showing that inclusive finance is the future of a thriving global financial ecosystem.

As the world’s financial ecosystems move increasingly online, global regulatory bodies are enforcing accessibility mandates that redefine standards for digital engagement. Here’s a closer look at the primary mandates propelling accessibility forward in finance.

| Country | Key Laws & Standards | Compliance Requirements | Year Enacted | Based On | Scope | Key Deadlines |

| Canada | Accessible Canada Act (ACA) | WCAG for public sector & large private companies | 2019 (ACA) | WCAG | Federal, provincial levels | Full accessibility for federally regulated entities by 2040; significant progress by 2025 |

| England | Equality Act 2010, Public Sector Bodies Accessibility Regulations 2018 | WCAG 2.1 for public sector websites & apps | 2010, 2018 | WCAG 2.1 | Public sector, reasonable adjustments for all | Public sector websites/apps compliance by September 23, 2020 |

| Germany | Federal Act on Equal Opportunities for Persons with Disabilities (BGG) | Public entities’ digital services must be accessible | Not specified | Not specified | Public entities | All public entities accessible by June 28, 2025, per EU Accessibility Act |

| France | Law for a Digital Republic | Public & private sector digital content must be accessible | Not specified | Not specified | Public & private sector | Compliance with EU deadline of June 28, 2025 |

| European Union | European Accessibility Act (EAA), Web Accessibility Directive (WAD), EN 301 549 standards | EU members to adopt by June 2022; enforced by June 28, 2025 | 2019 | WCAG, UN Convention | All digital products & services in EU | June 28, 2025 |

| United States | Section 508 of Rehabilitation Act, ADA, ACAA, CVAA | Federal agencies, businesses, nonprofits | Various | WCAG, Section 508 | Federal agencies, businesses, nonprofits | Ongoing; enforced through litigation and state-level requirements (e.g., CA, NY) |

| Singapore | IMDA Web Content Accessibility Guidelines | WCAG 2.0 for gov’t & private sector | Not specified | WCAG 2.0 | Gov’t & private sector | No specific deadline; ongoing encouragement for compliance |

| India | Rights of Persons with Disabilities Act, 2016 | RPWD Act & GIGW guidelines | 2016 | Not specified | All digital platforms | Ongoing enforcement; no specified deadline |

| Japan | JIS X 8341-3, Basic Act for Persons with Disabilities | WCAG 2.0 for gov’t websites | Not specified | WCAG 2.0 | Gov’t websites, ICT services | No specific deadline; regular assessments |

| Australia | Disability Discrimination Act (DDA) | WCAG endorsed by Human Rights Commission | 1992 | WCAG | All web content | No formal deadline; endorsed through Human Rights Commission |

| New Zealand | Human Rights Act 1993, NZ Disability Strategy, NZ Web Accessibility Standard 1.1 | WCAG 2.1 Level AA for public sector | 1993, updated later | WCAG 2.1 AA | Public sector websites | Ongoing with periodic reviews |

| Brazil | Brazilian Law of Inclusion (Law No. 13,146/2015) | WCAG 2.0 for public sector, encouraged for private | 2015 | WCAG 2.0 | Public sector, encouraged for private | Required for public sector since 2015 |

| Spain | Royal Decree 1112/2018 | WCAG 2.1 AA for large companies | 2018 | WCAG 2.1 AA | Companies >100 staff or €6M turnover | Compliance by September 2020 for qualifying private sector companies |

| Ireland | Disability Act 2005, Code of Practice 2006 | WCAG for public bodies | 2005, 2006 | WCAG | Public bodies | No specific deadline; ongoing for public sector |

| Italy | Law 4/2004 (Stanca Act) | WCAG 2.1 for public & many private | 2004, updated 2013, 2018 | WCAG 2.1 | Public sector, many private | Ongoing; updates in 2018 require compliance for public and some private sectors |

The consequences of non-compliance with accessibility standards in the financial sector are increasingly steep. With growing regulatory scrutiny worldwide, companies face a sharp rise in accessibility-related litigation. In the U.S., for example, ADA lawsuits tied to digital accessibility surged to over 3,500 cases in 2022 alone, marking a 14% increase from the previous year.

For banks and fintech companies, where trust and accessibility are foundational, these lawsuits bring high costs financially and in terms of consumer trust.

Consider Bank of America, which faced a significant accessibility lawsuit due to incompatibility with screen readers on its website. This case is far from isolated; other financial institutions, such as Wells Fargo, have also been cited in lawsuits for failing to accommodate users with disabilities.

High-profile cases like these not only lead to costly settlements but also risk undermining long-term brand credibility. Inaccessible digital platforms can lead to multimillion-dollar losses and a reputation for being unresponsive to the needs of diverse customer bases.

As the demand for accessible digital finance grows, so do consumers’ expectations. The pandemic accelerated digital adoption across all demographics, making accessible online banking and fintech services increasingly essential. Today, nearly 71% of users with disabilities report abandoning inaccessible websites—a rate that has risen from 57% in 2017.

Surveys consistently show that users with disabilities are quick to leave apps and websites that fail to meet accessibility needs, a trend that banks and fintech companies cannot afford to ignore.

The heightened demand for accessibility reflects a shift in the marketplace: consumers now expect inclusive design as a standard, not an exception.

In sum, non-compliance with accessibility standards is more than a regulatory risk; it’s a missed opportunity in today’s market. As financial institutions face rising legal, financial, and reputational costs, the demand for accessible digital banking signals that the future belongs to those who prioritize inclusivity.

Creating an accessible digital experience in banking and fintech is critical, yet it presents unique challenges due to the range of disabilities and needs that must be addressed. From visual impairments to cognitive and motor limitations, digital accessibility in finance requires thoughtful design that anticipates and accommodates diverse user experiences. The following are key accessibility challenges and real-world examples that highlight the importance of inclusive design.

Ensuring digital accessibility in finance is essential but challenging, given the diverse needs of users. Creating an inclusive banking experience requires thoughtful, user-centered design, from visual impairments to motor and cognitive limitations.

For users with visual impairments, accessibility issues such as poor color contrast, small font sizes, and inaccessible forms create barriers to effective navigation. Low-contrast color schemes, for example, make it difficult for users with color blindness or low vision to differentiate between interface elements, while small fonts can make critical information unreadable. Studies show that WCAG compliance issues—like the lack of alternative text, insufficient contrast, and complex CAPTCHAs—persist on many financial websites, creating significant usability challenges.

One solution is compatibility with screen readers like VoiceOver (iOS) and TalkBack (Android), which can interpret on-screen information aloud for users with low vision. Bank of America, for example, improved its mobile app with screen reader compatibility and larger text options, but not before facing legal action for previous inaccessibility.

Online banking interfaces are often dense with information, which can overwhelm users with cognitive impairments or neurodiverse needs, such as those with ADHD, dyslexia, or dementia. Complex navigation and cluttered layouts can lead to cognitive overload, where users struggle to focus, understand, or retain information.

Simplifying navigation, using plain language, and breaking down complex tasks into manageable steps can significantly enhance the experience for these users. Regions Bank, for example, has integrated simplified language and user-centered design into its digital services, making them accessible to users with cognitive impairments. These proactive efforts demonstrate how simplifying user interfaces can provide a more inclusive experience while benefiting all customers.

For users with motor impairments, tasks that require precise screen interactions, such as payments or account setup, can be challenging without appropriate keyboard-only navigation or accessible touch targets. Fintech platforms that rely heavily on mouse navigation or small interactive elements may alienate users who rely on assistive technologies or alternative input methods, such as switch access devices or voice commands.

To address this, many banks have started implementing large touch targets and keyboard-accessible interfaces. For instance, U.S. Bank’s mobile app offers voice command options and clear focus indicators, allowing users to complete actions without needing precise mouse control.

In regions with diverse linguistic backgrounds, accessibility must extend beyond language translation. Banking apps often lack multilingual support in regional dialects, limiting access for users who are more comfortable in their native language. In emerging markets, where mobile-first banking is common, digital platforms need to support local languages to ensure broad accessibility.

.

For instance, India’s State Bank of India (SBI) found that 72% of users over 60 struggled with the bank’s digital interface, partly due to language complexity and regional dialect barriers. To address this, SBI introduced localized language options to cater to users in rural and non-English-speaking regions.

As companies embrace inclusive design, they’re not only reaching new audiences but also solidifying a foundation for long-term success. Here’s how accessibility powers growth across key areas.

Digital accessibility opens doors to millions of potential users who previously faced barriers in accessing financial services. For instance, as populations age, more users require adaptable interfaces. By ensuring easy navigation, larger text options, and high-contrast visuals, banks and fintech companies can accommodate these users without alienating younger, tech-savvy customers.

HSBC, for example, found that by improving readability and simplifying its online banking app, it attracted more users over 50—an age group with growing financial influence and loyalty to accessible services.

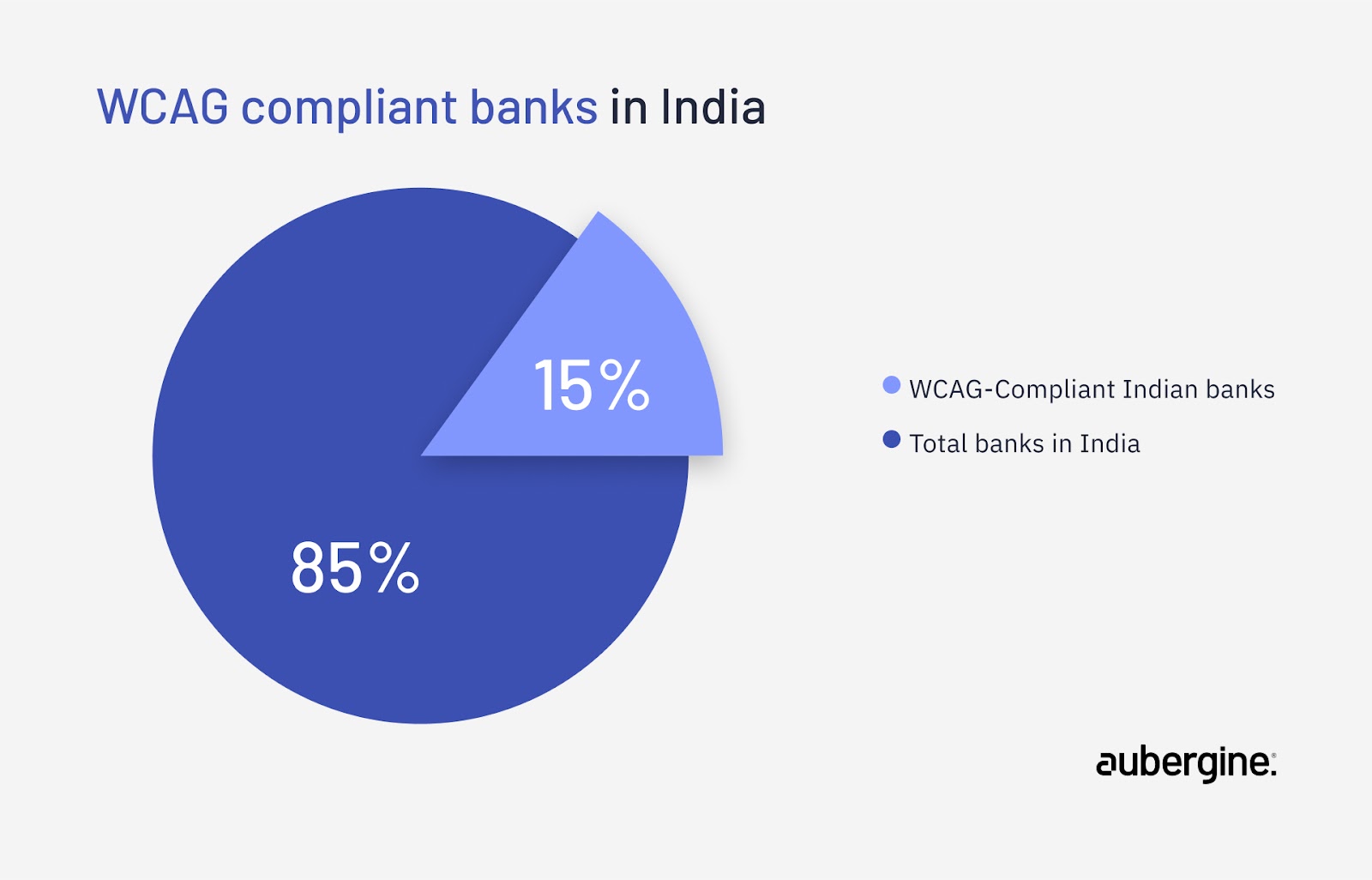

To grasp the profound impact of digital accessibility on users, let’s consider India as an example. As the world’s second-most populous country, India had over 6% of its population aged 65 and older in 2022, according to the World Bank. Despite this significant demographic shift, the growth in digital accessibility initiatives has not kept pace with the needs of this aging population.

For instance, only 15% of Indian banks meet WCAG compliance standards, highlighting a critical gap in ensuring equitable access to essential digital services for seniors.

Source: RBI

Similarly, a study by the Financial Health Network reveals that 71% of US customers aged 60 and older own a smartphone, with 94% using their devices daily. Interestingly, two-thirds of smartphone users over 50 do not engage in mobile banking, and the reasons for this limited usage still need to be clarified.

In the United States, individuals over 50 control 53.2% of the nation’s wealth, totaling $62.09 trillion, positioning them as a financially robust demographic. Banks should recognize this untapped potential and customize their digital offerings to meet their needs better. The benefits that drive banks to adopt digital solutions—cost-efficiency, operational effectiveness, and enhanced customer experience (CX)—are just as relevant for older adults.

For financial services, trust is the currency of customer loyalty. When companies prioritize accessibility, they communicate that they value every customer. Consider Regions Bank, which launched an accessible, sensory-friendly platform tailored for users with cognitive and sensory needs. By partnering with nonprofit organizations and directly engaging with users, Regions built a reputation as a trusted, inclusive bank, ultimately retaining customers who might otherwise have been underserved.

This trust has a measurable impact: users who feel that a company values inclusivity are more likely to remain loyal even if a competitor offers comparable services. In a world where trust is key to customer retention, accessible design becomes a strong loyalty driver.

Research consistently shows that users with disabilities are quick to abandon platforms that present barriers. In banking, where an inaccessible interface can mean the difference between a completed transaction and a lost customer, seamless design becomes vital.

Simple accessibility enhancements—like larger buttons, intuitive layouts, and voice command options—create a smoother experience, especially for users with motor or visual impairments. These adjustments can significantly reduce app abandonment rates, reinforcing a bank’s commitment to inclusivity and enhancing its reputation as a forward-thinking provider.

Prioritizing accessibility often sparks innovations that benefit all users. Features like automated text-to-speech and keyboard-only navigation, initially designed for users with disabilities, have become invaluable to multitaskers and mobile users who need quick, hands-free options.

In digital finance, elements such as transaction confirmations and guided navigation improve clarity and security for all customers, including those who may not rely on assistive tech but appreciate clear, user-friendly design.

One example from fintech is voice-activated commands in banking apps, which make transactions easier for users with limited mobility and appeal to busy professionals seeking hands-free options.

Additionally, customizable dashboards allow users to prioritize the information they need most, simplifying complex financial interactions. These accessible innovations demonstrate how inclusive design not only meets compliance but also creates a smoother, more engaging experience for every customer.

Finally, accessibility-driven companies often attract diverse talent, enhancing their innovative potential.

Studies show that inclusive workplaces foster higher engagement and satisfaction among employees, especially those who may have disabilities themselves. For companies like Salesforce, which places accessibility at the heart of its platform development, this commitment to inclusivity not only helps attract talent but creates a workplace where diverse perspectives contribute to a culture of continuous improvement

Creating an accessible digital finance platform requires more than essential compliance; designing a genuinely inclusive experience is necessary.

Creating a truly accessible digital finance platform starts with including users with disabilities from the outset. User testing with individuals with diverse needs—such as those with visual, cognitive, or motor impairments—ensures that essential features, including transactions, checkouts, and customer support, are genuinely accessible.

By involving these users early in the process, companies can gain firsthand insights into how people with disabilities interact with their platform, identifying barriers that may otherwise go unnoticed.

This approach brings several benefits. For one, it helps pinpoint functional gaps in navigation, labeling, and layout that standard testing might miss, allowing developers to address accessibility issues more effectively. Additionally, tackling these issues in the design phase significantly reduces the need for costly redesigns post-launch, saving time and resources in the long run.

Perhaps most importantly, designing with input from diverse users enhances overall user satisfaction. A user-centered approach leads to a smoother, more intuitive experience, boosting customer loyalty and positioning the platform as both inclusive and user-friendly.

| Accessibility Feature | Description | User Benefits |

| Keyboard-Only Navigation & Voice Commands | Enables users to navigate without a mouse, using keyboard shortcuts or voice commands. | Assists users with mobility impairments and visually impaired users |

| Clear and Intuitive Design | Simplifies layout and reduces visual clutter, making it easier to locate information. | Reduces cognitive load, helping users with cognitive disabilities and new users |

| Captioning and Audio Descriptions | Adds captions and descriptions to videos, providing alternative formats for multimedia content. | Supports users with hearing impairments by making content accessible |

| Ongoing Training and Awareness | Keeps development teams updated on WCAG standards and accessibility practices. | Ensures sustainable, compliant design and broadens team expertise |

| User-Centered Testing | Involves users with disabilities in testing stages to identify practical accessibility improvements. | Improves accessibility scores and reduces drop-off rates by refining user experience |

At Aubergine, we understand that accessibility in banking and fintech demands a nuanced, sector-specific approach that addresses complex regulatory requirements, enhances usability, and promotes sustainable growth. Our accessibility framework is designed to guide clients from initial compliance to an enduring culture of inclusivity. Here’s how we make it happen:

Our accessibility audits are crafted with banking and fintech needs in mind, focusing on critical areas such as secure authentication, transaction accessibility, and overall usability of digital services. By examining these elements in detail, we identify key improvement areas that directly impact both compliance and customer experience, offering clients a highly customized pathway to accessibility.

Accessibility is not a one-time fix; it’s an ongoing commitment. That’s why Aubergine offers an enduring partnership model to support clients in maintaining and enhancing accessibility over time. Through continuous updates, strategic guidance, and an adaptable roadmap, we help banks and fintech platforms stay compliant while fostering a culture of inclusivity and innovation.

Aubergine implements its custom, in-depth accessibility framework across Visual, Content, and UX categories, which forms the cornerstone of our comprehensive evaluation methodology and robust assessment and recommendation process.

Our comprehensive evaluation covers both tech and design parameters, ensuring complete accessibility assessment coverage beyond traditional audits focused solely on WCAG guidelines. This holistic approach helps businesses create truly inclusive and user-centric digital experiences.

Once issues are identified, we create a data-driven roadmap that prioritizes improvements based on user impact, severity and the feasibility of resolution. This approach allows our clients to implement changes that deliver immediate, high-value returns, focusing resources where they will make the most significant difference to both compliance and user satisfaction.